Newsletter December 2025

As we approach the end of 2025, we reflect on another eventful year both in global markets and geopolitically

Both the UK and U.S. equity markets navigated a dynamic landscape. Central banks maintained their focus on achieving a balance between growth and inflation, with the Federal Reserve and Bank of England adjusting their monetary stances in response to evolving economic conditions. The incoming Trump administration introduced new policy expectations around trade, taxation, and regulation, at times creating uncertainties for investors. Meanwhile, the UK worked through the implications of Labour’s fiscal policies introduced in late 2024, which continue to influence business sentiment and economic activity.

In this newsletter, we bring updates on global markets from both a U.S. asset manager and a UK fund manager’s perspective, provide an update on changes to U.S. citizenship applications, highlight U.S. tax reporting requirements for foreign assets, and summarise announced changes to how and when UK expatriates can make future UK State Pension contributions.

As always, please do not hesitate to contact your Florin Pensions advisor if you have any questions regarding your UK pension.

Everyone at Florin Pensions would like to wish you and your families a joyful holiday season and a prosperous New Year.

Margetts Fund Management:

Monthly Diary November 2025

Commentary

The top three performing IA sectors in the month of November were IA North American Smaller Companies (1.04%), IA UK Direct Property (0.62%), and IA Global Equity Income (0.57%). The bottom three performing IA sectors over the month were IA Asia Pacific ex Japan (-3.24%), IA Global Emerging Markets (-2.61%), and IA UK Smaller Companies (-1.87%).

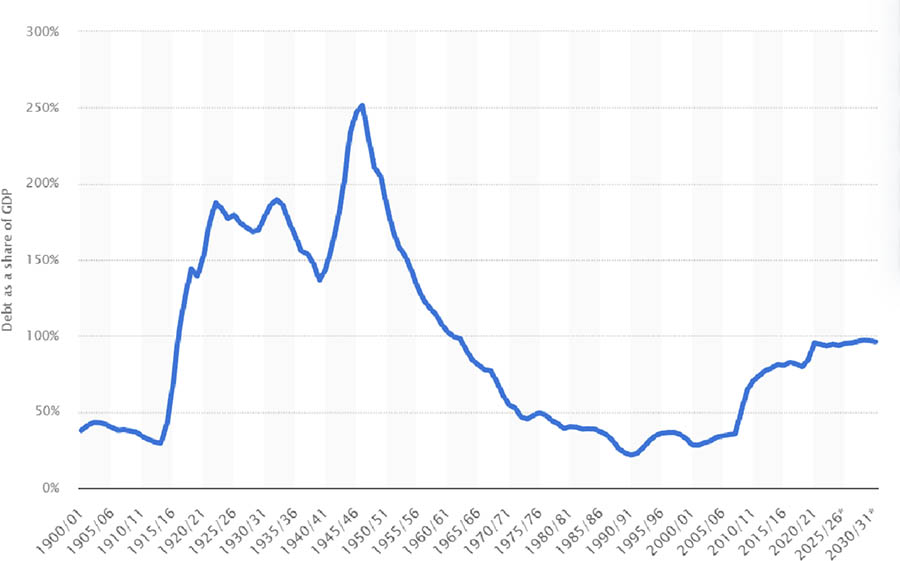

Following the global financial crisis and COVID-19 pandemic, the UK’s public debt now stands at levels not seen since the aftermath of the Second World War. In the 1940s, debt peaked at over 250% of GDP before decades of growth and inflation gradually eroded the burden. Today, the ratio is far lower than that historic peak, but still alarmingly high by modern standards, and interest payments alone consume more than 4% of annual GDP.

Public sector net debt as a percentage of GDP in the United Kingdom1

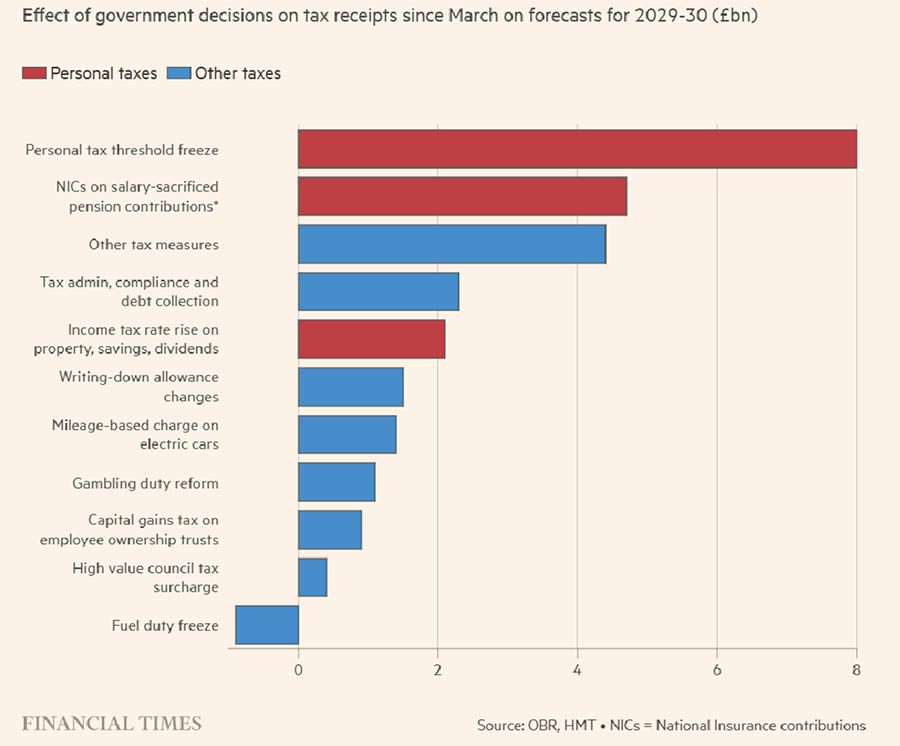

The Autumn budget delivered by Rachel Reeves (with spoilers delivered by the OBR) took this debt position into account. Reeves unveiled £26 billion in additional tax measures, taking the tax-to-GDP ratio to a 40-year high². The bulk of this comes from freezing income tax thresholds until 2031, which will drag millions into higher bands over time. Other measures include hikes on dividend and property income, a mansion tax on homes over £2 million, and tighter pension salary-sacrifice perks.

The Chancellor largely avoided headline rate hikes, but the extended freeze on tax bands means fiscal drag will do the heavy lifting. This approach is politically easier but economically contentious, as it erodes disposable income and could dampen consumption. For investors, this signals a prolonged environment of higher effective taxation on households, albeit with the bulk of personal taxes not kicking in untll 2028.

Effect of government decisions on tax receipts since March on forecasts for 2029-30(£bn)3

However, market participants seemed largely satisfied with the budget. It avoided extremes of being too fiscally loose and addressed the UK debt position. While the reaction also suggested it wasn’t too fiscally tight and didn’t overly inhibit growth. UK gilt yields dipped modestly, and sterling rallied against both the dollar and the euro following the announcement. The pound climbed to around $1.32 and €1.14, while 10-year gilt yields eased to roughly 4.4%.

While the budget passed the market test, the popularity of the Chancellor and her party continues to struggle. Tax hikes never win popularity contests and history reminds us why. After the War of the Roses, Henry VII inherited a broken England and rebuilt confidence through institutional reform, waves of taxation and disciplined spending. It worked financially, but when Henry died, his passing was met with celebrations by nobles and commoners alike. Unsurprisingly, consumers in an economy hate taxes and dislike the people who hike them.

This is the second tax-hiking budget from Reeves. This originated from a manifesto that promised not to raise taxes on “working people.” The last one was prescribed as essential to fill the black hole in public finances, but this one will seem more invasive to “working people” and more down to Labour’s own mismanagement. Consumer confidence remains low with further uncertainty around the next budget moving the goalposts. A recent survey by the British Retail Consortium found that card spending fell 1.1% year on year in November, the largest fall since February 2021.

The OBR downgraded productivity growth by 0.3 percentage points per year following the budget. Pointing towards a reality that tax tweaks alone won’t solve the UK’s structural challenges. While the budget changes leave capital investment and infrastructure spending untouched, the absence of supply-side reforms leaves questions about how Britain will escape its low-growth trap. One solution may come from the Bank of England, who are expected to cut rates in December and three more times in 2026. This would bring the base rate down to around 3%, providing a tailwind for borrowing costs and opening greater possibilities of capital expenditure from businesses.

The Autumn Budget had the task of acknowledging the UK’s heavy debt position without choking off growth. Reeves introduced significant tax measures, but most won’t bite until 2028 and could be reversed if the outlook improves. Markets welcomed stability, potentially on a ‘it could have been worse’ basis, yet uncertainty looms large. Labour’s U-turns on manifesto pledges, like PIP payments and income tax changes, raise questions about credibility. For consumers and business owners, the real risk isn’t today’s tax hikes but tomorrow’s unpredictability. If confidence falters, spending and investment will suffer.

Footnotes

1. UK government debt 2025 | Statista

2. UK government revenue as GDP 2025 | Statista

3. Budget in brief: what you need to know

Important Information

Please note that the contents are based on the author’s opinion and are not intended as investment advice. This information is aimed at professional advisers and should not be relied upon by any other persons. Any research is for information only, does not constitute financial advice or necessarily reflect the views of the author and is subject to change. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the fund is suitable and appropriate for their customer. Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise and investors may get back less than they invested especially in the early years. Important information about the funds can be found in the Supplementary Information Document and NURS-KII Document which are available on our website or on request.

|

Toby Ricketts CEO, Margetts Fund Management Ltd. |

U.S. Citizenship Rule Changes: Why Green Card Holders Wanting U.S. Citizenship Should File Now

In the weeks following the 2024 election, I began sharing periodic reminders on social media encouraging green card holders wanting to apply for U.S. citizenship to file their applications sooner rather than later. This is particularly the case for green card holders who are already considered long-term residents from a U.S. tax perspective. My instinct was clear: change was coming. What I could not fully predict, however, was the speed, scope, and intensity with which those changes would arrive.

Today, the naturalization landscape has shifted even more dramatically than many anticipated. Long-standing norms are being reconsidered, application requirements are tightening, and the overall processing environment has become increasingly unpredictable.

Most notably, U.S. citizenship applications have just undergone substantial procedural and substantive revisions. These developments signal a new era of scrutiny and complexity in the naturalization process, one that will directly impact eligibility, timelines, and outcomes for countless lawful permanent residents.

Reinstated Neighborhood Investigations

In August 2025, USCIS issued a policy memorandum introducing new standards for adjudicating naturalization applications. In one of the most significant, yet largely underreported, changes, USCIS reinstated neighborhood investigations for naturalization applicants. This marks the first meaningful return to this practice since the early 1990s and represents a clear tightening of scrutiny in citizenship adjudications.

USCIS has long held the authority to investigate an applicant’s reputation within their community by speaking with neighbors, employers, colleagues, and others familiar with the applicant. These investigations focus on the five years preceding the N-400 filing and are used to verify:

- Continuous residence

- Good moral character

- Attachment to the Constitution

- A positive disposition toward the United States

For decades, these investigations were largely replaced by fingerprinting and FBI background checks. Now, USCIS is ending its broad waiver and reintroducing this tool on a case-by-case basis.

Naturalization applicants should now anticipate possible requests for:

- Testimonial letters from neighbors

- Statements from employers or co-workers

- Evidence of community reputation

Applicants who cannot provide such evidence, or whose cases raise concerns, may face a neighborhood investigation, which has the potential to delay or complicate their application.

Heightened Good Moral Character Review

In a separate August 2025 memo, USCIS also updated its Good Moral Character (GMC) adjudication standards. The agency continues to apply the preponderance of the evidence standard, and serious offenses such as murder, aggravated felonies, torture, and genocide remain permanent statutory bars to establishing GMC.

USCIS is now placing renewed emphasis on ensuring that naturalization reflects both allegiance and character. Officers must evaluate the totality of an applicant’s life, not merely the absence of misconduct. Positive factors will now carry greater weight, including:

- Long-term community involvement

- Family responsibilities and caregiving

- Educational achievements

- Stable and lawful employment

- Lengthy lawful residence

- Sound financial responsibility

At the same time, officers will scrutinize negative conduct more closely. This includes statutory issues such as DUIs or false claims to citizenship, as well as broader behavior falling short of community norms, such as habitual reckless driving, harassment, or other patterns of concerning conduct.

Since these policies are so new, we will have to wait and see how they unfold in practice.

A New Civics Test Began October 20, 2025

Finally, USCIS updated the naturalization civics test in September 2025. The agency will administer the new 2025 Civics Test to all applicants who file Form N-400 on or after October 20, 2025.

The new test is an oral exam that includes 20 questions selected from 128 possible questions and requires at least 12 correct answers to pass. Applicants who filed before October 20, 2025, will continue to take the 2008 civics test.

The Takeaway: If You Qualify, File Now

If you qualify and would like to apply for U.S. citizenship, it is best to apply at your earliest opportunity. Those who act now will be far better positioned as USCIS implements these changes nationwide. The path to citizenship remains open, but the process is evolving quickly. Acting sooner, not later, may make all the difference.

Notes:

- When considering whether or not to apply for U.S. citizenship, I also recommend that you consult a U.S. tax advisor in advance to understand any U.S. tax implications for your particular circumstances.

- In addition, while the United Kingdom permits dual citizenship, some countries do not. It is therefore important to confirm whether your home country allows dual citizenship before applying, as acquiring a new nationality may require you to renounce your existing one.

|

Tahmina Watson Founder of Watson Immigration Law |

Do You Have U.S. Tax or Foreign Reporting Requirements?

In today’s global economy, U.S. individuals and businesses are increasingly expanding across borders, opening foreign bank accounts, forming overseas entities, investing internationally, or even relocating from country to country.

When it comes to non-U.S. assets, the U.S. government wants to know two things: (i) where are your assets and (ii) are you paying U.S. taxes from the income the assets generate?

In order to get this information, U.S. taxpayers must report not only their worldwide income, but also their worldwide financial assets.

To ensure compliance, Congress enacted significant penalties for non-compliance. For example, a failure-to-file FBAR penalty can be up to $10,000 per violation.

U.S. taxpayers with international financial interests face a complex web of reporting requirements, and understanding the key forms is essential for compliance and avoiding steep penalties.

Here are a few of the most common reports that deserve attention:

FBAR (Foreign Bank Account Report)

The FBAR requires U.S. persons, including citizens, residents, and certain entities, to report foreign financial accounts if the aggregate value exceeds $10,000 at any point during the year. These accounts include bank and brokerage accounts, mutual funds, pensions, and even accounts where the filer has signature authority but no ownership.

FBAR is often confused with FATCA, but they serve different purposes. FBAR is filed with FinCEN and applies to accounts over $10,000, while FATCA is filed with the IRS and covers broader foreign assets starting at $50,000. Many taxpayers are required to file both; more on this is covered in the next section.

The filing process is straightforward: submit FinCEN Form 114 through the BSA E-Filing System. The deadline is April 15, with an automatic extension to October 15, and records must be kept for five years.

Penalties for non-compliance are severe. Non-willful violations can result in fines up to $16,536 per violation, while willful violations can lead to penalties of $165,353 or 50% of the account balance per violation. Criminal penalties may include fines up to $250,000 and five years in prison, with harsher consequences for aggravated cases.

Common misconceptions include ignoring accounts with zero balances, thinking the $10,000 threshold applies on a “per account” basis, forgetting accounts with signature authority, and assuming FATCA filing satisfies FBAR requirements.

FATCA Reporting (Form 8938)

Form 8938, officially called the Statement of Specified Foreign Financial Assets, was introduced under the Foreign Account Tax Compliance Act (FATCA) to increase transparency and reduce offshore tax evasion. Unlike the FBAR, which is filed with FinCEN, Form 8938 is attached to your annual federal income tax return and filed with the IRS.

Similar to FBAR, you must file Form 8938 if your foreign financial assets exceed the applicable thresholds. However, unlike the FBAR, these thresholds vary by filing status and residency. For taxpayers living in the U.S., the threshold is $50,000 at year-end or $75,000 at any time during the year for single filers, and $100,000/$150,000 for married filing jointly. For those living abroad, the thresholds are much higher: $200,000/$300,000 for single filers and $400,000/$600,000 for joint filers.

Form 8938 generally has a broader scope than the FBAR. Reportable assets include foreign bank and brokerage accounts, foreign-issued stocks and bonds, interests in foreign partnerships or trusts, and certain foreign pensions.

Similar to the FBAR, failure to file can result in steep penalties: $10,000 for non-compliance, with additional $10,000 increments every 30 days after IRS notification, up to $50,000.

Foreign Trusts & Large Foreign Gifts (Form 3520)

Often, taxpayers receive gifts or bequests from a non-U.S. person or estate. Generally, the receipt of a gift or bequest is not taxable in the U.S. However, for those receiving large gifts or bequests from foreign individuals or entities, Form 3520 is required if the value of the gift or bequests exceeds $100,000.

This reporting obligation is strict and often overlooked, and late filing can trigger penalties of up to 25% of the gift’s value. The form requires detailed information about the donor and the gift, and aggregation rules apply for related parties.

Form 3520 is also used to report certain transactions with a foreign trust. These include creating or transferring property to a foreign trust, being treated as the owner of a foreign trust under the grantor trust rules, or receiving distributions, whether cash, property, or even indirect benefits such as loans or use of trust-owned property.

The form is filed separately from your income tax return, but it shares the same due date: April 15, with an extension to October 15 if your tax return is extended.

Owner of Foreign Corporations (Form 5471)

If you are a shareholder in a foreign company, you probably need to file Form 5471. Form 5471 is used to disclose ownership and financial details of foreign corporations to ensure compliance with U.S. international tax rules, including Subpart F and Global Intangible Low-Taxed Income (GILTI) provisions introduced by the Tax Cuts and Jobs Act (TCJA).

There are various different categories of Form 5471 filers. Each category requires specific sections of the Form 5471 to be filled out.

The form is filed with your annual income tax return by the regular due date, including extensions. It requires extensive detail, including ownership structure, financial statements, earnings and profits, and related-party transactions.

Penalties for non-compliance are severe. The initial penalty is $10,000 per foreign corporation per year for failure to file or filing an incomplete return. If the failure continues after IRS notice, additional penalties of $10,000 per 30-day period apply, up to $50,000 maximum.

International tax compliance is complex. If you think any of these forms might be applicable to you, please contact your U.S. tax advisor to discuss your filing obligations.

|

Moses Man Founder of M Squared Tax PLLC |

What Lies Ahead in 2026? Some Thoughts on the Outlook for Markets and the Economy

Market Strategy Radar Screen (December 14, 2025)

For a third year in a row, we expect stocks stateside to experience a broadening of the powerful rally that began early in the fourth quarter of 2022 and has persisted since, notwithstanding some interruptions as counterpoints to its upside trajectory.

“We maintain our call to overweight exposure to U.S. equities into

2026 as we continue to expect the U.S. economy and markets to

lead the world economy into some kind of a new normal.”

Looking back over the last few years, we recall that the upside trajectory that emerged in late 2022 came about after the market had become significantly oversold on expectations of economic and earnings recessions that were ultimately never realized.

Since that earlier recovery, the market has undergone numerous periods that have included what seems like relentless day-to-day upside for stock prices and expanding valuations across sectors. These were followed with some regularity by periods of selling fed by some catalyst worthy of consideration that appeared in the markets, providing bears, skeptics, and nervous investors to take some profits in stocks intermittently without FOMO (fear of missing out) amidst what in hindsight now appears to have been a longer-term bull market.

A Detour Need Not Be a Journey End

Ironically, the downside produced by some catalysts that prompted nervous selling created opportunities for more bullish investors to “catch the babies that got thrown out with the bathwater” (good stocks caught in market downdrafts). Repeatedly over the last few years, once the catalyst to sell has been discounted, some positive data or news flow has come along to reassert an upside move in the market. We expect this process of selective buying on dips will continue, and we see periods of near-term weakness in some sectors that illustrate it.

The effect overall has been a positive development for the markets in keeping both bulls and bears on their toes. While past performance is certainly no guarantee of future results, we have found that the modern market, steeped in the Bernanke legacy of Fed transparency and frequent communication, serves to discount both good news and bad news more quickly than we can recall over the course of a little more than 42 years in the markets. While we do not expect the current pattern will go on endlessly, nor do we think that trees grow to the sky, for now, the persistence of the good fundamentals that have carried the bull case from October 2022 remains intact and is likely to remain supportive in the year ahead.

These positive fundamentals that overcame the periods of turbulence experienced over the last few years, we find persistent in the current landscape and in our view are included in a mix of monetary policy, fiscal stimulus, resilient economic earnings, and consumer growth, along with what appears to be watershed innovation that is not likely to plateau soon.

The Gains From Tech Should Benefit All Sectors

Ultimately, the markets move higher on revenue and earnings growth, both of which appear to be in good standing based on past seasons’ results, which have improved over the course of the last few years. Earnings season surprises across the sectors beyond technology and communications services over more than just a few quarters suggest to us that the broadening in investor interest across the sectors is not solely for diversification but is a prudent avoidance of concentration in just a few sectors, or market capitalization or style buckets but also a move to gain exposure to companies that can benefit from the innovation that percolates out of technological innovation and improvements.

Corporations that engage tech to generate greater efficiencies will likely attract investors and customers in the year ahead and for some time in the future as AI and its usage expand. An increase in technology investments across non-tech-related sectors should boost efficiencies and productivity, enhancing their attractiveness.

The relatively attractive valuations of sectors outside the sectors that harbor the so called “Magnificent Seven” should contribute to a further broadening of the rally, as well economic growth that appears sustainable stateside.

Don’t Forget the Fed

Monetary policy by the Federal Reserve is likely to be supportive of higher bond prices as the central bank moves closer to the end of the current rate hike cycl,e should inflation remain steady or slide further towards the Fed’s 2% inflation target. Inflation’s stickiness factor remains to be put in check.

For now, it is our view that the Fed is not likely to accelerate the pace of rate cuts it has thus far undertaken since last year. While a change of leadership is expected at the Fed when Jerome Powell’s successor takes the helm, there is little, if any, indication that the Fed will lessen its dependency on economic data in its deliberations. This year’s 75 bps in total cuts versus last year’s 100 bps in reductions supports our view that the pace of easing is slowing.

We maintain our call to overweight exposure to U.S. equities into 2026 as we continue to expect the U.S. economy and markets to lead the world economy into some kind of a new normal.

Economic growth should also remain resilient in our view as the effect of the Big Beautiful Bill factors into the economic mix sometime next year. For now, we rightsize our expectations for U.S. GDP, looking for economic groups similar to what we experienced this year, with periods of weakness offset by periods of surprising strength.

Where We Stand Now

We remain positive on stocks and regard them as our favorite asset class. We continue to favor cyclical sectors over defensive sectors. Our favorite sectors include: information technology, communications services, industrials, financials, and consumer discretionary. Regarding the consumer discretionary sector, we note that while surveys of consumer sentiment (soft data) reflect concern by the consumer near term related to inflation and the health of the economy, the hard data or sales data persist in showing that the consumer continues to shop, if somewhat selectively and at a slower pace reflective of some sensitivity to prices.

Beyond our aforementioned favorite sectors, the utilities sector should garner increased favor as interest rates move lower. The sector is considered by many investors as a bond proxy that can benefit when interest rates move lower.

The sector also has appeal as a thematic sector with prospects for the revitalization of the U.S. electric grid, a necessity as AI and other technologies increase the demand for electricity.

In our view, portfolio diversification among asset classes held in portfolios remains an important consideration to meet the needs, goals, objectives, and tolerance to risk of private investors and the needs of mandate driven institutions in an environment which remains in transition on a number of levels including: technological innovation, fiscal policy, monetary policy, geopolitical, and domestic politics around the world. Fixed income remains, in our view, complementary to stocks as a source of income and for diversification among primary asset classes.

Stay tuned

|

John Stoltzfus Chief Investment Strategist, Managing Director Jim Johnson, Senior Director |

Autumn Budget 2025 Update: Changes to UK National Insurance Contributions for UK Expatriates

Whilst the UK press continued to speculate heavily about potential changes to the UK pensions’ landscape in the Autumn Budget 2025, such changes did not thankfully materialise. However, one unexpected change was announced regarding UK expatriates’ ability to continue to make UK National Insurance (NI) contributions while abroad.

Starting from the 2026-27 UK tax year, UK expatriates will no longer be able to pay voluntary Class 2 NI contributions for periods spent abroad. Only voluntary Class 3 contributions will be available.

This change results in a significant increase in the annual cost for UK expatriates wishing to make UK NI contributions whilst living or working abroad. For the 2025-26 tax year, Class 2 contributions cost £182 annually, whereas Class 3 contributions cost approximately £920 per year — nearly five times more expensive for the same State Pension benefit.

According to HMRC, these changes are being made to ensure that individuals building a State Pension from outside of the UK have a sufficient link to the UK and are paying a fairer price to do so.

New Eligibility Requirements

From April 2026, individuals wishing to make voluntary Class 3 contributions from abroad must satisfy one of the following conditions:

- Have lived in the UK for a continuous period of 10 years, or

- Have paid at least 10 years of National Insurance contributions while resident in the UK.

These requirements represent a significant tightening of eligibility criteria and are designed to ensure individuals have a sufficient connection to the UK before building up UK State Pension entitlement from overseas.

Prior to this announcement, individuals living abroad and/or working abroad could pay voluntary Class 2 or voluntary Class 3 National Insurance contributions if they had either:

- Previously lived in the UK for 3 years in a row, or

- Paid at least 3 years of National Insurance contributions.

Important Protections

The new changes do not affect voluntary contributions made for periods abroad before 6 April 2026. UK expatriates can continue to pay for historical years under the previous rules and rates.

If you are currently making Class 2 Contributions:

- HMRC will contact affected individuals from July 2026

- Final Class 2 payments for the 2025-26 tax year will be collected on 10 July 2026 for those paying by Direct Debit

- It is recommended that contributors should not cancel Direct Debit arrangements prematurely

If you are currently making Class 3 contributions, there is no need to reapply to continue to make payments.

Application Process

Applications for voluntary Class 3 contributions from abroad can continue to be made using Form CF83.

What Steps Can Be Taken Now?

HMRC has noted that further detailed guidance and transitional arrangements will be published at a later date. However, at this time, it is well worth reviewing your UK NI record to identify any gaps before April 2026.

Where eligible, you can pay voluntary contributions to fill in any NI gaps going back 6 years. The deadline is 5 April each year.

It is also important to assess whether you will meet the new 10-year residence or contribution requirement being introduced.

Happy Holidays from the Florin Pensions team